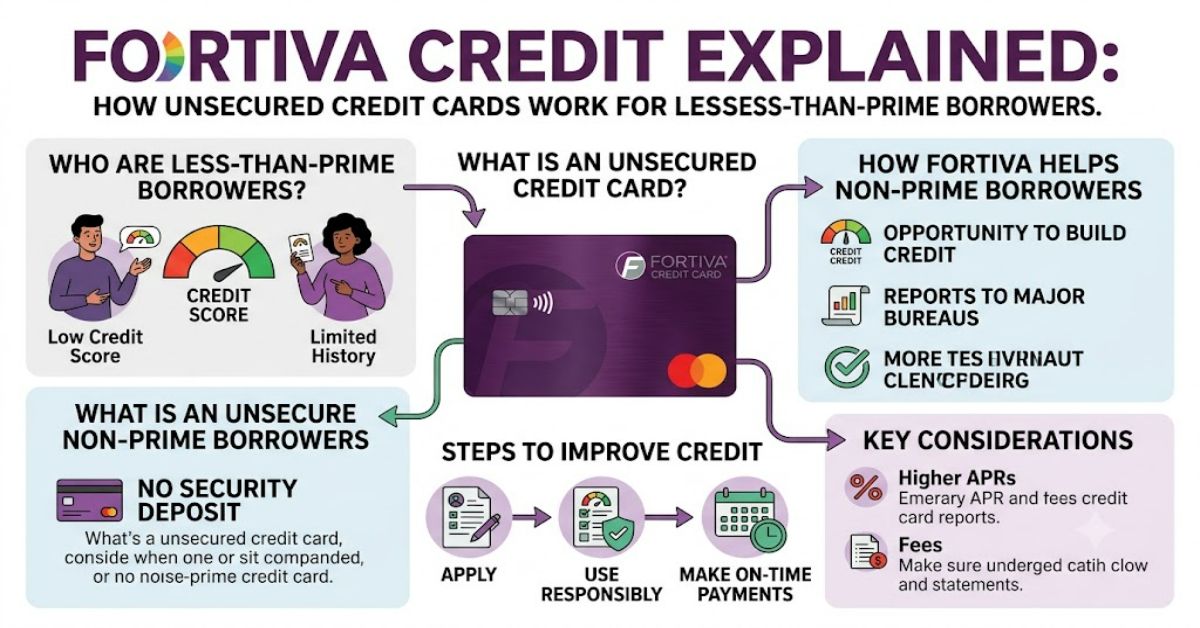

Fortiva is a financial services brand associated with unsecured credit cards and retail financing solutions aimed at consumers who may have difficulty qualifying for traditional credit products. Unlike secured cards that require a cash deposit, Fortiva Credit products generally provide access to revolving credit without requiring collateral.

For individuals rebuilding their financial position, these products can represent an opportunity to establish payment history and improve credit visibility. However, they also require careful evaluation because credit products designed for higher-risk borrowers often include higher annual percentage rates (APRs), account fees, and stricter cost structures than mainstream credit cards.

The demand for alternative credit solutions has increased as millions of consumers continue to face challenges accessing affordable borrowing. According to the Consumer Financial Protection Bureau (CFPB), credit access remains closely connected to credit scores, income stability, debt levels, and previous repayment behaviour.

Understanding how Fortiva works requires looking beyond approval availability. Consumers need to examine the complete lending structure, including fees, reporting practices, repayment terms, and whether the product supports their wider financial goals.

For borrowers with limited credit histories, the right financial product can become a stepping stone towards stronger credit opportunities. However, poor repayment management can increase financial pressure rather than solve existing challenges.

This analysis examines Fortiva’s business model, advantages, limitations, consumer impact, and what borrowers should consider before using unsecured credit products.

How Fortiva Credit Works

Fortiva operates within the alternative credit market, where financial providers serve consumers who may not meet the lending requirements of major credit card issuers.

Traditional lenders often rely heavily on credit scores, income verification, debt-to-income ratios, and established borrowing histories. Consumers with previous missed payments, limited credit history, or financial disruptions may find approval more difficult.

Unsecured credit products work differently because they do not require a security deposit. Instead, lenders manage risk through:

- Credit limits

- Interest rates

- Account fees

- Payment monitoring

- Credit reporting relationships

Fortiva’s target market typically includes consumers seeking access to credit while rebuilding their financial profile.

The product structure reflects a wider trend in financial services: expanding credit availability while managing increased lending risk.

The Role of Alternative Credit Providers

Alternative lenders have become increasingly relevant because traditional credit scoring systems do not always capture a consumer’s complete financial situation.

For example:

- A young adult with limited borrowing history may have a low score despite reliable income.

- Someone recovering from past financial difficulties may need several years of positive payment history to regain access to mainstream credit.

- Consumers without extensive banking relationships may require different pathways into financial products.

Alternative credit providers attempt to fill this gap by using different risk models and focusing on consumers who represent higher lending risk.

Fortiva Credit Cards Compared With Other Credit-Building Options

Consumers considering Fortiva should compare it with other available methods of establishing or rebuilding credit.

| Credit Option | Requires Deposit | Typical User | Main Advantage | Main Limitation |

| Fortiva unsecured credit card | No | Less-than-prime borrowers | Easier access without collateral | Higher potential costs |

| Secured credit card | Yes | Credit beginners | Lower risk for lenders | Requires upfront cash |

| Traditional credit card | No | Established borrowers | Better rates and rewards | Harder approval |

| Credit-builder loan | Usually no | Credit-building consumers | Builds repayment history | No immediate spending access |

The key difference is that unsecured alternative credit provides immediate purchasing capability but transfers more lending risk into pricing structures.

Costs, Fees and Financial Trade-Offs

One of the most important factors consumers should evaluate is the total cost of borrowing.

Higher-risk credit products commonly involve:

- Higher APRs

- Annual fees

- Lower initial credit limits

- Reduced rewards compared with premium cards

The advertised credit limit is not the only measure of value. A card with a higher limit but expensive fees may create more financial strain than a lower-cost product with fewer features.

Example Cost Consideration

| Factor | Consumer Impact |

| High APR | More expensive carried balances |

| Annual fees | Increased account cost |

| Late payment charges | Additional financial pressure |

| Low credit limit | Higher utilisation risk |

| Regular payments | Opportunity to build positive history |

A borrower who pays the balance in full each month may reduce interest exposure. Someone who carries balances over multiple billing cycles may experience significantly higher costs.

Credit Reporting and Long-Term Financial Impact

A major reason consumers choose products like Fortiva is the possibility of improving their credit profile.

Credit scores are influenced by several factors, including:

- Payment history

- Credit utilisation

- Length of credit history

- Credit mix

- New credit applications

Payment history is one of the most significant scoring factors. Consistently paying on time can demonstrate reliability to future lenders.

However, simply opening an account does not automatically improve credit. Poor management, missed payments, and high balances can negatively affect financial progress.

Practical Credit-Building Strategy

A disciplined approach generally includes:

- Paying every bill before the due date

- Keeping balances low compared with available credit

- Avoiding unnecessary applications

- Monitoring credit reports regularly

- Increasing savings alongside credit development

Real-World Consumer Considerations

Financial products aimed at less-than-prime borrowers exist because millions of consumers face barriers in traditional lending markets.

The Federal Reserve’s household finance research has repeatedly shown that many households experience unexpected expenses, income instability, or limited emergency savings. These conditions often influence borrowing behaviour.

For consumers, credit access can provide benefits such as:

- Managing unexpected costs

- Establishing financial history

- Improving future borrowing opportunities

However, credit access alone does not solve underlying financial challenges. Without budgeting discipline, additional borrowing may increase debt burdens.

Hidden Risks Consumers Should Understand

Several less obvious issues deserve attention before applying.

1. Credit Availability Does Not Equal Affordability

Approval may create the impression that borrowing is manageable, but affordability depends on income, expenses, and repayment capacity.

A credit limit should not be treated as available income.

2. Higher Costs Can Delay Financial Recovery

Consumers rebuilding credit may already face financial pressure. Expensive borrowing can slow progress if balances remain unpaid.

3. Small Credit Limits Can Increase Utilisation Ratios

Credit scoring models consider utilisation. A borrower using most of a small credit limit may appear riskier, even when payments are made on time.

Fortiva Compared With Mainstream Credit Cards

| Feature | Fortiva-Type Credit Products | Mainstream Credit Cards |

| Target customer | Less-than-prime borrowers | Established borrowers |

| Approval standards | More flexible | More selective |

| Interest costs | Often higher | Usually lower |

| Rewards | Limited compared with premium cards | Wider rewards programmes |

| Credit-building purpose | Common objective | Secondary benefit |

This comparison highlights the trade-off between accessibility and cost.

Consumers who qualify for mainstream products may find cheaper alternatives, while those rebuilding credit may value accessibility more highly.

Market Impact of Alternative Credit Services

The growth of alternative credit providers reflects wider changes in consumer finance.

Digital applications, automated underwriting, and financial data analysis have changed how lenders assess borrowers.

Technology allows companies to:

- Process applications faster

- Analyse repayment patterns

- Offer specialised products

- Reach underserved groups

However, regulators continue examining consumer protection issues surrounding high-cost credit.

In the United States, agencies including the CFPB have focused on transparency, fair lending practices, and clear disclosure of borrowing costs.

Structured Insight Table: What Consumers Should Evaluate

| Evaluation Area | Key Question |

| Cost structure | How much will borrowing actually cost annually? |

| Repayment ability | Can monthly payments fit comfortably within income? |

| Credit goals | Will the product support long-term improvement? |

| Alternative options | Are cheaper products available? |

| Spending habits | Will credit reduce or increase financial stress? |

The Future of Fortiva Credit in 2027

The future of alternative credit products will likely be shaped by technology, regulation, and changing consumer expectations.

Artificial intelligence-based underwriting is becoming more common across financial services, allowing lenders to analyse broader financial information. However, regulators continue to emphasise responsible lending and consumer protection.

By 2027, credit providers are expected to face greater pressure to provide:

- Clearer pricing information

- Better digital account management

- More personalised financial tools

- Stronger consumer education resources

The direction of the industry will depend on balancing two priorities: expanding credit access while preventing harmful borrowing patterns.

Alternative credit products are likely to remain important because many consumers will continue needing pathways into mainstream financial systems.

Key Takeaways

- Fortiva serves consumers who may have difficulty accessing traditional credit products.

- Unsecured credit provides convenience but may involve higher costs.

- Responsible repayment behaviour is essential for building stronger credit profiles.

- Borrowers should compare total costs rather than focusing only on approval.

- Alternative credit providers help expand financial access but require careful consumer evaluation.

- Credit improvement depends on long-term financial habits, not only opening new accounts.

Conclusion

Fortiva represents a segment of the financial services market focused on improving credit access for consumers who may not qualify for traditional lending products. Its unsecured credit model offers convenience because it does not require collateral, but accessibility often comes with higher borrowing costs and careful repayment requirements.

For consumers, the value of such products depends largely on how they are managed. Used responsibly, an alternative credit product can help establish payment history and support future financial opportunities. Poor repayment decisions, however, can increase financial pressure.

Understanding fees, interest rates, credit reporting practices, and personal affordability remains essential before applying. As financial technology continues developing, alternative credit providers will continue playing a role in connecting underserved consumers with financial services while facing increasing expectations around transparency and responsible lending.

Frequently Asked Questions

What is Fortiva used for?

Fortiva provides unsecured credit products designed mainly for consumers who may have difficulty qualifying for traditional credit cards. It can be used for purchases and, when managed responsibly, may support credit-building goals.

Is Fortiva a secured or unsecured credit card?

Fortiva primarily refers to unsecured credit products, meaning approval does not typically require a refundable security deposit.

Can Fortiva help improve credit scores?

A Fortiva account may contribute to credit improvement if payments are made consistently and balances are managed carefully. Credit improvement depends on overall financial behaviour.

Why are alternative credit cards more expensive?

Alternative credit cards often serve higher-risk borrowers, so lenders may charge higher interest rates or fees to manage increased lending risk.

Should someone with poor credit apply for Fortiva?

Consumers should compare costs, repayment ability, and other available options before applying. The product should fit within a realistic financial plan.

How does Fortiva compare with secured credit cards?

Secured cards require deposits but often have lower risk for lenders. Fortiva-style unsecured products provide easier access without requiring upfront collateral.

Methodology

This article was prepared using publicly available information from financial regulators, consumer finance research organisations, and industry documentation. Sources were reviewed to understand alternative credit markets, consumer lending practices, and credit-building principles.

The analysis considers both potential benefits and limitations of unsecured credit products. Individual product terms, fees, and approval criteria may change over time, so consumers should review current agreements directly before making financial decisions.

This article was drafted with AI assistance and requires editorial verification of all financial claims, regulatory references, and product-specific information before publication.

References

Consumer Financial Protection Bureau. (2024). Consumer Credit and Lending Markets Report. Washington, DC: CFPB.

Federal Reserve Board. (2024). Economic Well-Being of U.S. Households in 2023. Washington, DC: Board of Governors of the Federal Reserve System.

Federal Trade Commission. (2024). Credit and loans: Understanding your options. Washington, DC: Federal Trade Commission.

Office of the Comptroller of the Currency. (2023). Fair lending and consumer protection guidance. Washington, DC: OCC.

Editorial Note: All statistics, product terms, regulatory references, and financial claims should be independently verified against current primary sources before publication.

{kind=link}